By Bryan Perry, new Eagle Financial Publications Investment Expert

Historical records for the major averages continue to be set on an almost monthly basis, with the Nasdaq nearing its former all-time high of 5,000 thanks primarily to the strength of Apple (AAPL). Apple’s market capitalization now exceeds a staggering $800 billion. In a market such as this one, when historical valuation comparisons are cast into the wind, it becomes clear that momentum investing has taken hold of the landscape.

The mighty move up for the U.S. dollar is drawing fund flows from all over the world. Investors are seeking to tap into the look and feel of an unstoppable bull market in equities and equity income-based assets. The closely watched weekly American Association of Individual Investors (AAII) sentiment survey shows bullish optimism climbing to 45% and bearish pessimism dropping to 20%, both of which are extreme readings that have a very good track record of being contra-indicators. In other words, investors are overly complacent and the market is due for a pullback.

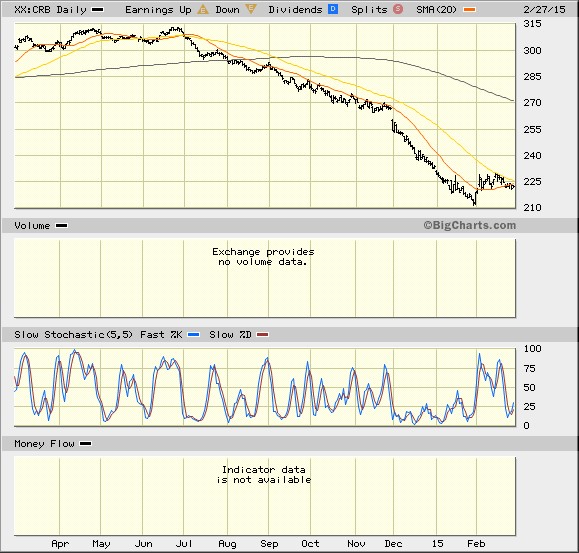

The latest round of “Fed speak” from Janet Yellen would have us believe that until the rate of core inflation rises to 2.0%, investors shouldn’t expect a rate hike of any degree. My take on the use of the word “patient” in the most recent Federal Open Market Committee (FOMC) minutes is that it’s telling in that there may not be a hike in the Fed Funds rate this year at all. All one has to do is take a gander at the broad commodities market as measured by the Commodities Research Bureau (CRB Index), where a picture says a thousand words and it becomes glaringly clear that deflation is a bigger threat than inflation.

Assuming the Fed is on hold for the foreseeable future, the business of investing for dividend income maintains its front-row status among professional and retail investors alike. While the 10-year Treasury Note is paying a paltry yield of 2.01%, the SPDR S&P 500 ETF (SPY) is paying only 2.15% following a run up to 2,100 for the broad market index. That return may not excite you, but fortunately there is a buffet table of high-yield alternative asset classes where 5%, 10%, 15% and even upwards of 20% yields can be garnered.

My Cash Machine investment newsletter incorporates a wide variety of high-yield securities to generate a blended yield in excess of 10%. Many of those positions offer monthly payouts for income investors to appreciate while allowing them to participate in the secular bull market for stocks. In fact, roughly 90% of the holdings within the current portfolio are tied to the equity markets with nominal exposure to the bond market and the risk associated with higher interest rates.

Some of the places where generous yields can be harvested against the current investing landscape are in convertible debt, specialty real estate investment trusts (REITs), Master Limited Partnerships (MLPs), Business Development Companies, Buy/Write Covered Call Closed-End Funds, Asset and Private Equity Managers, Floating Rate Debt and Exchange-Traded Notes. These types of hybrid securities target various market sectors and give investors a diverse approach to generate income.

Regardless of whether the Fed stands pat on rates, investor sentiment is heavily skewed to the view that the Fed will begin to raise short-term interest rates later this year. Therefore, concise asset selection for income investors seeking outsized yields is at a premium. The mantra at Cash Machine of “strategic high-yield investing” couldn’t be more appropriate at a time when massive rotation out of fixed income will be looking for a new home that is sensitive to an improving economy, gradual inflation and a tighter Fed policy.

One such high-yield asset that fits this profile is Calumet Specialty Products Partners L.P. (CLMT), an MLP and a leading independent producer of specialty hydrocarbon and fuels products that is enjoying the tailwinds of low crude oil prices. The company posted fourth-quarter 2014 results on Friday that were very impressive. The Partnership’s specialty products and fuel products segments reported significant growth in adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) during the fourth quarter when compared to the prior-year period. Primary reasons for the growth stemmed from a combination of improved reliability at the partnership’s key fuels refineries and a significant year-over-year decline in crude oil prices that contributed to improved margins, particularly within its specialty products segment.

During fourth-quarter 2014, specialty products gross profit increased $26.3 million. Distributable Cash Flow (DCF) for fourth-quarter 2014 was $38.2 million, compared to $10.6 million in the prior-year period. For the full year of 2014, DCF was $142.9 million, compared to $18.5 million in 2013. These much-improved profits translate to a healthy distribution coverage of 1.9x and more than support the annual $2.74/share payout to provide a 9.8% current yield. This is exactly the kind of stock that high-yield income investors should be buying. It also is what makes the Cash Machine investing model so special.

In case you missed it, I encourage you to read my e-letter column from last week about why the Fed won’t raise rates right away. I also invite you to comment in the space provided below my Eagle Daily Investor commentary.

{kind=link}